This article first appeared in City & Country, The Edge Malaysia Weekly on March 31, 2025 – April 6, 2025

Malaysian property developers are optimistic that demand will pick up in the second half of the year, according to an industry survey by the Real Estate and Housing Developers’ Association (Rehda) Malaysia.

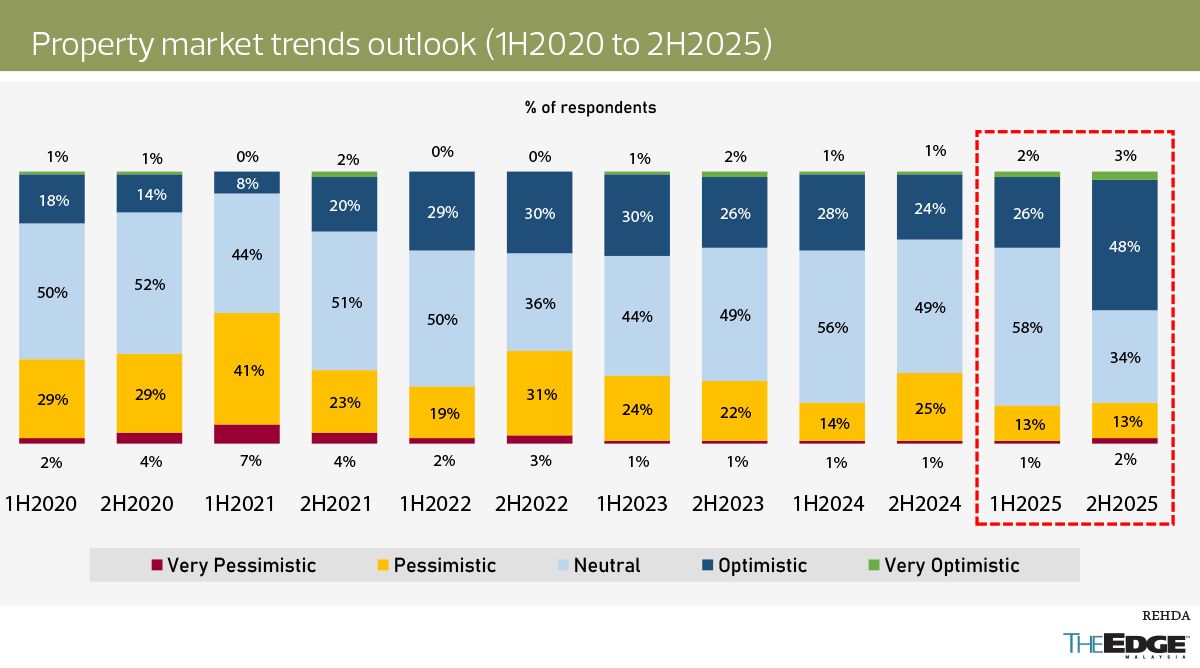

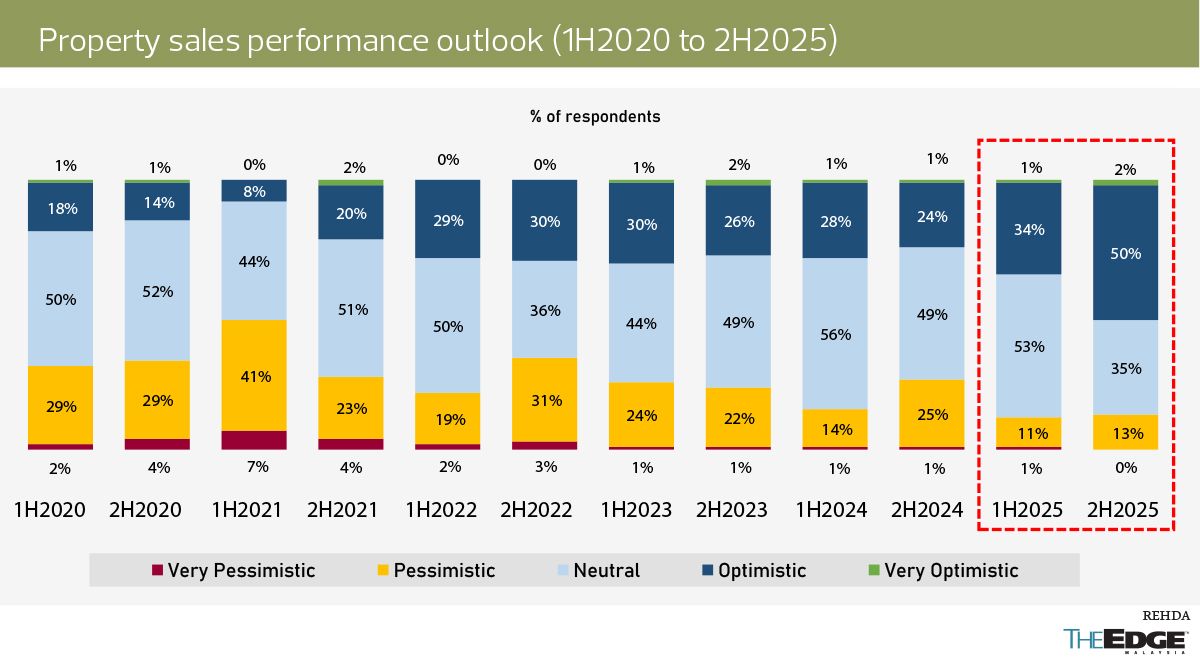

More than half of the respondents in the survey expressed increased confidence in property market trends and sales performance for 2H2025, with 51% feeling optimistic (48% optimistic, 3% very optimistic) about trends and 52% confident (50% optimistic, 2% very optimistic) about sales performance.

This contrasts with just 28% (26% optimistic, 2% very optimistic) and 35% (34% optimistic, 1% very optimistic) for the first half of 2025. According to Rehda president Datuk Ho Hon Sang, who presented the survey results during a media briefing at Wisma Rehda in Petaling Jaya on March 20, overall optimism is at its highest level in five years.

“There is more optimism about the second half of 2025 because of economic-spurring initiatives such as the Johor Bahru-Singapore Rapid Transit System (RTS) Link, Johor-Singapore Special Economic Zone, National Energy Transition Roadmap and New Industrial Master Plan 2030,” said Ho.

He added that homebuyers and developers are waiting to see how these initiatives will drive the property industry.

“Perhaps for 1H2025, the timing is not good enough. They believe that these projects and initiatives can drive better performance later in the year, for instance, in the second half. The many festivals in 1H2025 could also be another factor [for the reduced optimism in property sales].”

The latest edition of the Property Industry Sentiment Survey drew responses from 127 members of Rehda in Peninsular Malaysia.

“While the outlook for 1H2025 is slightly more optimistic than for 2H2024, we can see that the respondents are very optimistic about the second half of this year, with nearly twice the amount of optimism, signalling that they are expecting better times ahead,” said Ho.

In terms of business outlook, he noted that it was a mixed bag, with 46% of respondents wanting to hire more in the next 12 months, compared with 49% who were looking to freeze hiring and 5% who were considering a reduction in the size of their workforce.

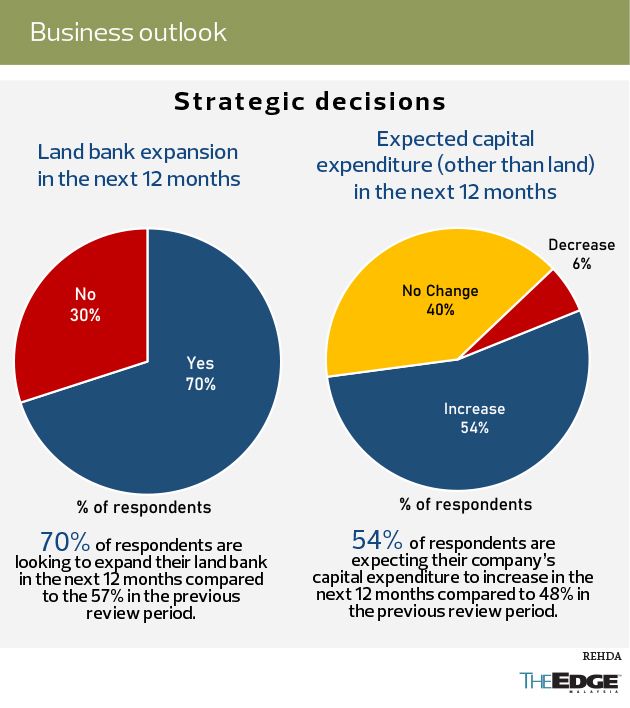

Meanwhile, 70% of respondents said they were looking to expand their land bank in the next 12 months compared with 57% in the previous review period (1H2024). As for capital expenditure, 54% of respondents were expecting their company’s capital expenditure to increase in the next 12 months compared with 48% in 1H2024.

Challenges abound

Despite the optimism, there are still “a lot of worries” in the industry due to the various challenges stakeholders face, said Ho. He attributed these concerns to utility price hikes, petrol subsidy rationalisation, unexpected taxes and the cost impact of conditions imposed by various agencies, which are expected to drive costs higher.

He was presenting the results of another Rehda survey — the Property Industry Survey 2H2024 & Market Outlook 2025 — which saw the participation of 177 Rehda members.

Most developers (73%) reported a 3% to 6% increase in expenses in 2H2024, the survey found. Additionally, 56% of developers flagged construction challenges, including rising material costs, supply shortages and labour constraints.

In the meantime, 37% of the respondents indicated that they were affected by the economic conditions in 2H2024, while 52% were neutral about it.

“Among the cost-cutting measures were a freeze in recruitment, fewer benefits or perks, rescheduling of planned launches and a reduction in the scale of launches,” said Ho.

“While the government is working to address supply and labour shortages, these challenges are becoming increasingly costly for both the industry and the wider economy. We understand that the government is doing its best to address the issues of building materials and labour, but we hope that the government is also cognisant that these will be more costly to deal with the longer they go on, not just for the industry but for the economy as well.”

Some 68% of respondents faced financing issues, with three-quarters of them citing end-financing as the main issue in 2H2024.

“The top three factors affecting end-financing loan rejection are ineligibility of buyers’ income, inadequate financial documentation and adverse credit history,” explained Ho.

Meanwhile, 11% of the developers (out of the 68%) reported issues with bridge financing. According to Ho, they cited the bank’s requirement of additional documents, higher sales required before drawdown (between 10% and 60%) and the development of price-controlled housing as the main factors.

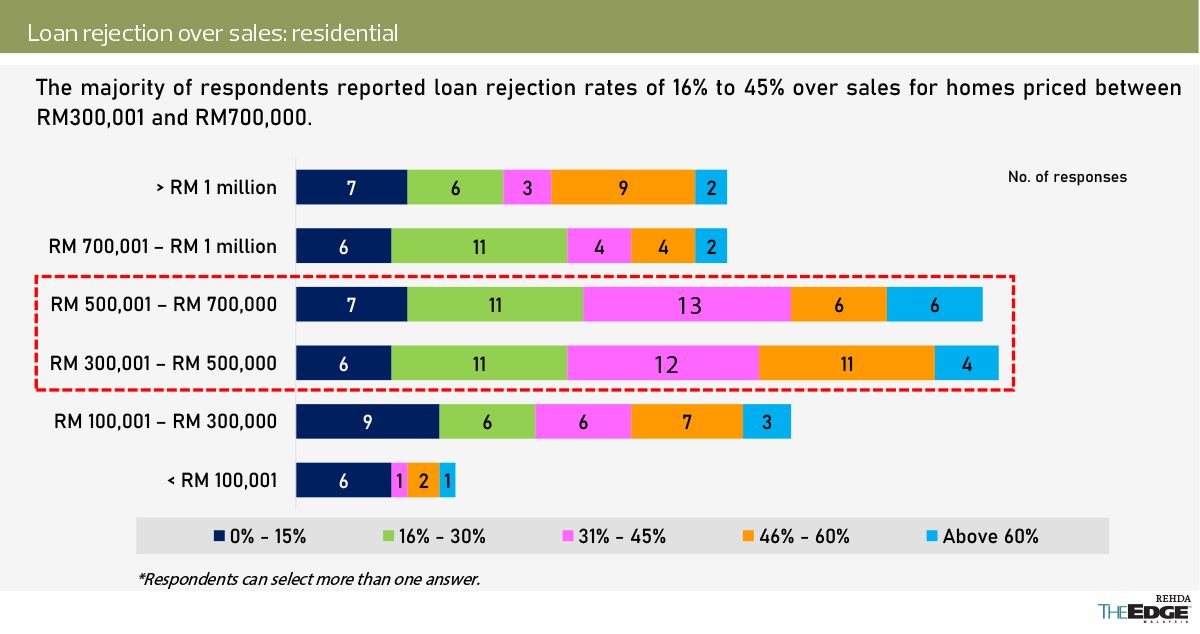

In terms of price range, the majority of respondents reported loan rejection rates of 16% to 45% over sales for homes priced between RM300,001 and RM700,000, he said.

When it comes to price-controlled housing, the top three challenges faced by developers are difficulty in maintaining profitability due to price caps (26%), delayed approval process and bureaucratic hurdles (18%), and meeting regulatory requirements and compliance standards (15%).

“Nevertheless, developers are employing strategies such as optimising layout and design, implementing efficient construction methods and reducing their profit margin. These are quite standard strategies that need to be adopted. Although they are standard, one would require talent and experience in the organisation for them to be effectively implemented,” said Ho.

Unsold housing units

As for unsold completed residential units, Ho mentioned that the main reasons were end-financing loan rejection (25%), low demand or interest (19%) and the high pricing of the residential units (16%).

The survey also found that 41% of the respondents had unsold completed residential units at the end of 2024.

Most of the overhang units were priced between RM400,001 and RM500,000, and more than half of them (55%) were serviced residences, followed by single-storey terraced houses (16%) and condominium units (8%).

“Fifty per cent of the unsold units had been completed between 13 and 24 months,” said Ho.

Future launches

In terms of future launches, 56% of the respondents planned to launch their projects in the first half of this year.

“For those who do not plan to do so, they have cited reasons such as delays in approval, unfavourable market conditions, business constraints and shortage of land bank, among others,” said Ho.

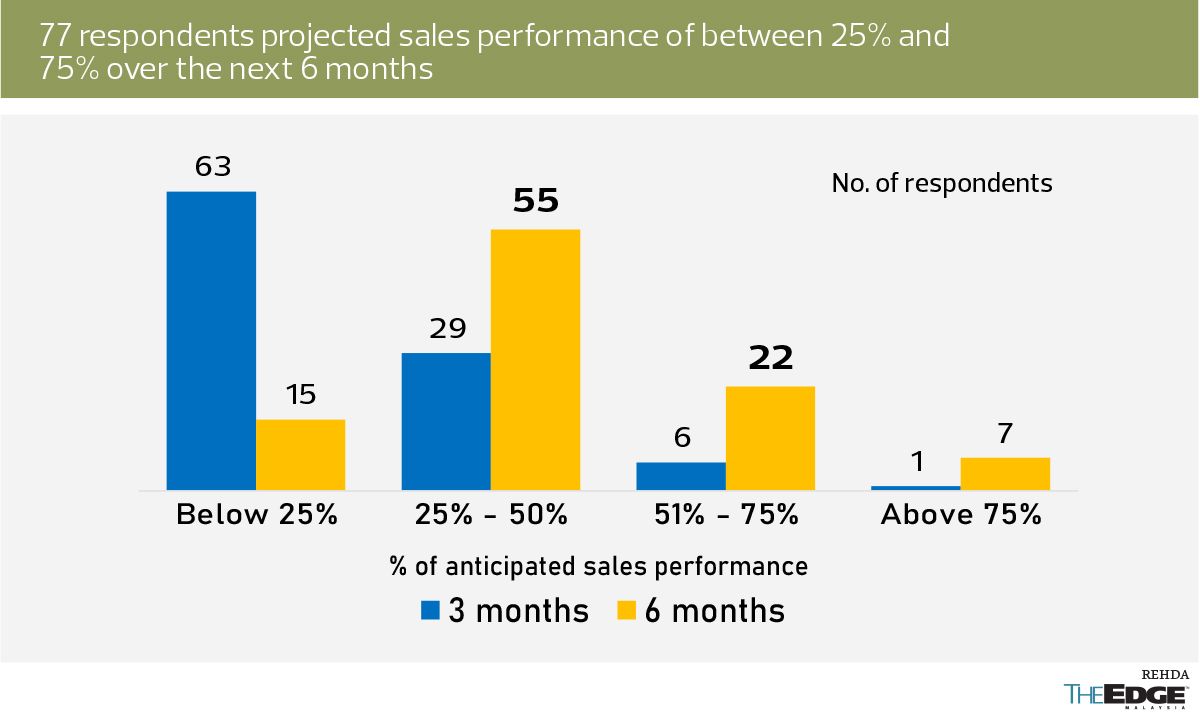

He added that 77 of the respondents projected sales performance of between 25% and 75% over the next six months. Furthermore, an estimated 9,805 landed residential and 11,828 strata residential units are expected to be launched in 1H2025.

Green agenda getting stronger

The majority of the developers agreed that green buildings are an effective way to improve the environmental performance of the property and construction sector, with the survey showing that 72% agreed.

Additionally, 28% of respondents developed up to five green-certified projects between 2015 and 2024.

“Most respondents that developed green-certified projects used the GreenRE rating system, averaging two projects per developer. The green agenda is getting stronger and stronger,” said Ho.

“The feedback that we are getting [from developers] is that green buildings translate into energy savings and reduced operating costs, improved project profile and company branding, as well as better financing incentives such as a slightly more attractive interest rate.”

Despite that, he noted that there are still cost implications in implementing green projects, coupled with the lack of government incentives and limited public awareness.

Save by subscribing to us for your print and/or digital copy.

P/S: The Edge is also available on Apple’s App Store and Android’s Google Play.