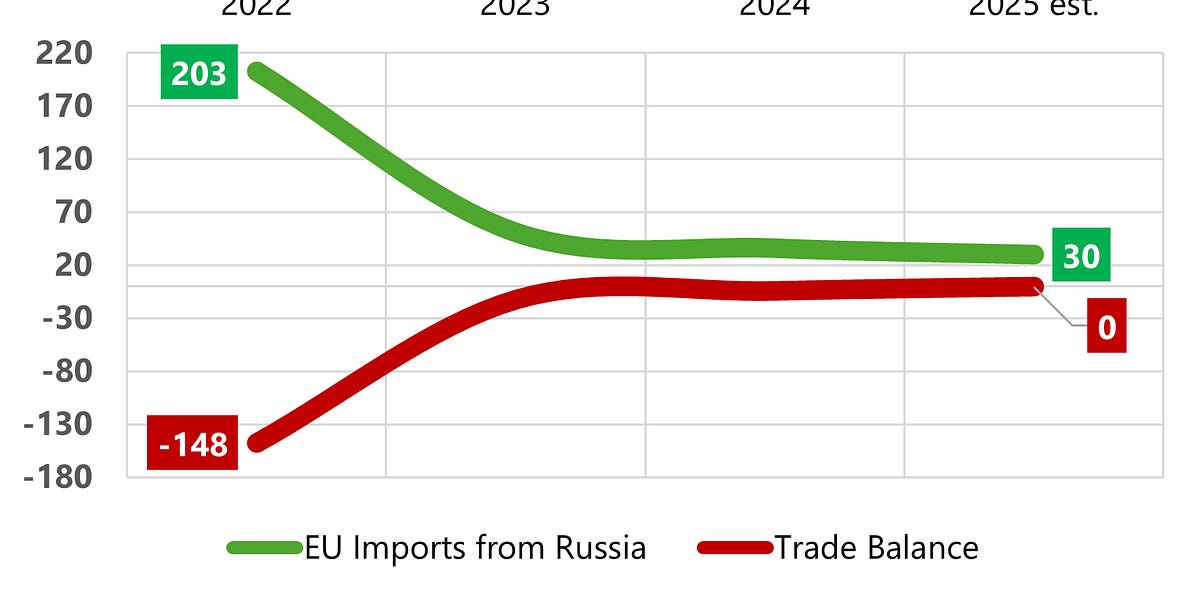

From an all-time high trade deficit with Russia to zero in just three years. Said and delivered

After Russia invasion, imports from Ukraine fell off a cliff, while Russian exports to China jumped to record highs.

Draghi’s Rimini speech didn’t sound like summer musings. He ticked off the threats one by one: China backing Russia, the war in Ukraine, industrial overcapacity spilling into Europe, U.S. tariffs, and the EU looking like the weak flank. It didn’t come across as a rant either. More emotion than we usually hear from Draghi, sure, but still too structured to dismiss as beachside chatter

Best to call it a rant with a purpose, perhaps to argue that the EU should issue common debt to cope with Russia, Ukraine, China, and, as if that wasn’t enough, the Trump sequel.

China’s surplus is easy to describe but harder to interpret. Despite rhetoric about self-reliance, frequent references to the “Global South,” and self-congratulatory claims about the role of net exports, the reality is more nuanced and domestic propaganda tends to sidestep it.

For 2025, we forecast China’s total goods surplus at about $1.2 trillion (customs basis), up 19% from 2024 and a new high. By our estimates, nearly $1 trillion still comes from advanced economies, which cuts against the narrative of a pivot away from the West. At the same time, China records a large surplus with the Global South, roughly $0.45 to 0.50 trillion. The contrast is stark: Beijing speaks of “win-win cooperation,” yet the pattern remains an asymmetric balance in China’s favor.

These headline figures are partly offset by familiar deficits. We estimate about $139 billion with Taiwan (chips and integrated circuits), $57 billion with Australia (minerals and ores), and $23 billion with Russia (energy, mainly crude). Net of these deficits, the surplus still totals about $1.2 trillion.

The strategic rub is this:

Sustaining large surpluses with the Global South has limits, including thinner household incomes, debt stress, and rising local protection. On the Western front, the current turmoil raises the risk of anti-dumping and anti-subsidy duties, EV tariffs, tighter investment screening, and export controls. China has leverage in scale and supply chains, but the West can also run out of patience.

Can Beijing afford to strain both fronts at once when the advanced economies still provide most of the surplus that supports reserves and export employment? Running both fronts is costly and risky for Beijing, but we doubt China’s leadership will change course.

One last contrast. Beijing spotlights the “three new productive forces” of batteries, electric vehicles, and photovoltaics. Yet, our estimates suggest that the export value moving through cross-border online platforms shipping low-cost consumer goods (Temu, Shein, and the like) is now comparable to the combined exports of those three sectors. The headlines focus on high tech, but much of the cash still comes from mass-market low prices.

China acknowledges the numbers in the graph, but it relentlessly contests their meaning. Whatever explanation the EU advances, Beijing shifts the blame onto European political choices rather than its own economic model. For the EU, meeting China these days is nothing but predictable futility.

Four years ago, for every €100 the EU exported to the U.S., it exported €56 to China. By 2025, for the same €100 to the U.S., EU exports to China will have fallen to just €31.

On any comparative measure, whether amounts, instruments, loans, land or policies, Chinese shipbuilding stands out as one of the most heavily subsidized industries in the country. Whether it is the most subsidized is difficult to judge, but it unquestionably belongs in the top tier.

Yet despite massive state support, the record over two decades shows that in dollar terms China’s ship export volumes have been essentially flat. The boom years of 2005 to 2014 produced 206 billion dollars in exports. The following decade, 2015 to 2024, yielded almost the same at 207 billion dollars.

That symmetry, 206 billion versus 207 billion, tells the story. Even with huge subsidies and industrial reorganization, the sector drifted through much of the 2010s, a lost decade, managing only in the 2020s to claw its way back to its earlier peak.

The next decade will be defined less by China’s ship export value than by its command of the global fleet. For the U.S., Europe, Japan, and South Korea, the real worry is not the money China makes but the dependency it creates.

In essence, today’s trade figures do not signal a healthy partnership. They reflect a distressed borrower, Venezuela, drawing down the last remnants of a long-expired credit line from its largest creditor, China. The arrangement is secured by the forced sale of natural resources.

With the apparent window of relief from the U.S. now slammed shut, the recent uptick in China–Venezuela trade looks fragile, squeezed between geopolitical headwinds and Venezuela’s heavy debt overhang. Most estimates say Venezuela still owes China between $10 and $20 billion.

For China, this looks less like economics and more like politics. The debt may never be fully repaid, but it guarantees China both leverage and a foothold in the region. Further restructuring seems inevitable. SOAPBOX readers will recognize the pattern: this is simply China being China.

On August 25, BYD announced that its plant in Thailand had shipped the first batch of DOLPHIN electric vehicles to the EU and UK markets, totaling just over 900 units. A fully manufactured EV from Thailand (not just assembled) faces a 10% EU tariff, compared with a punishing 35% if made in China.

BYD also has plans for a factory in Hungary, which would enjoy zero tariffs inside the EU, and another in Turkey, which like Thailand would be subject to 10% tariffs. What remains unclear is which models BYD intends to produce in Hungary or Turkey.

Our sense is that BYD, just in case, is hedging its bets on all fronts. Notwithstanding this, we are certain that rules of origin will be scrutinized closely to prevent diversion through third-party production hubs.

January–July 2025 exports are down 15% year over year despite the increase in July.

China continues to push ahead with state-backed efforts to develop EUV lithography, yet it remains years behind Dutch leader ASML. The current turmoil only makes those ambitions harder to realize, especially with ASML set to roll out next-generation lithography tools in 2026 that will push the gap even wider.

Chinese exporters of Christmas goods pulled shipments forward this year amid tariff worries. By end-July, exports were nearly 20% higher than a year ago. The chart, however, points to fatigue: the bump looks more like precautionary front-loading than genuine growth.

China’s imports of liquefied natural gas (LNG) from Russia are roughly ten times larger than its imports from the United States. In contrast, the EU’s LNG imports from the U.S. are already four times larger than from Russia, and the gap keeps widening.

We are committed to sharing with you the best trade analysis we have to offer.

If you would like to share something with us, feel free to comment in the section below or drop us a line at [email protected]

Like this:

Like Loading…

Нашия източник е Българо-Китайска Търговско-промишлена палaта