Amid the challenges facing China’s property market, work is well under way to restore confidence in the housing sector. It remains an uphill task for both Beijing and the country’s property groups, but there are signs of renewed investor interest in the Chinese property bond market as the housing sector’s outlook is expected to improve.

China’s property market drama: the boom and bust

There are countless mantras about how we ought to live our lives. “成家立业”, loosely translated as “start a family and build a career”, is one such expectation. However, these “guidelines” are essentially social narratives that may have been shaped without present-day people in mind. There is one desire that still resonates with many modern-day individuals—the pursuit of homeownership. Owning a home, even for those who have little time for traditional family formation and values, has been lauded as the best investment for one’s savings and a ticket to wealth. However, this dream of homeownership is crumbling fast. A historical note: China’s property market has been a key pillar of the economy (and it still is) ever since former paramount leader Deng Xiaoping began opening its markets in the 1980s. In 1998, the government encouraged private housing ownership and investment, instead of state-owned housing that was the norm before1998. The demand for housing has never been stronger.

And so, riding on the property boom that powered the country’s relatively recent economic miracle, millions of Chinese poured their life savings into real estate as they moved from the countryside into the cities and climbed the property ladder. Home buyers often pay upfront for unfinished projects. However, prices in many cities eventually became unaffordable for the average worker, prompting Beijing to impose limits on borrowing by developers based on balance sheet metrics. This initiative, known as the “Three Red Lines”, aimed to deleverage the real estate industry and tackle the housing bubble.

The property boom came to a crashing halt in 2021 when giant property developer Evergrande defaulted. This was followed by a string of defaults by other smaller, indebted developers and plunged the market further into crisis, leaving swathes of idle construction sites and uncompleted homes. The COVID-19 pandemic complicated matters by hammering consumer confidence. Demand for new housing fell and oversupply problems were exacerbated.

Since then, the Chinese government has made several positive overtures towards the real estate sector, but the effectiveness of these actual interventions remains a subject of debate.

China’s bid to stabilise its property market

Beijing’s response to the crisis was to relax previous regulations that restricted many potential homebuyers in order to boost home purchase transactions, improve market liquidity and lift overall confidence. However, the slew of piecemeal property easing measures implemented until the end of 2023 fell short of market expectations and created uncertainty regarding the country’s determination and approach to stem its property slump. In fact, the prices of new homes in major Chinese cities fell at the fastest pace in almost nine years in December 2023.

However, 2024—seven years after President Xi Jinping declared that “houses are for living in, not for speculating”—marked a radical shift in China’s property policies. The country’s top brass stepped up easing efforts in a more coordinated and comprehensive manner to revive its debt-stricken property sector. Here is a brief recap of the developments throughout 2024 for those who may have become lost in the mountain of property measures unveiled.

On top of continued demand-side property easing measures, 2024 marked a radical shift towards increasing efforts to improve property developers’ access to financing. The year kicked off with the launch of “Project Whitelist” initiative, allowing city governments to recommend residential projects to banks as being suitable for quicker lending and financial support. This initiative aimed to improve delivery of presale homes and ease liquidity squeeze faced by developers. Furthermore, the use of proceeds (UOP) from commercial property-backed loans was expanded to enable developers to repay debts.

In May 2024, People’s Bank of China (PBOC) established a Chinese renminbi (RMB) 300 billion relending facility to support local governments in purchasing completed unsold housing inventory for conversion into affordable housing, shortly after the Politburo called for efforts to clear “excess housing inventory” at the end of April. The minimum down payment ratio for individuals’ commercial housing mortgages was also lowered from 20% to 15% for first-home purchases, and the mortgage floor rate was abolished across the country.

In September 2024, Guangzhou became the first top-tier Chinese city to fully lift restrictions on home purchases, while Shanghai and Shenzhen announced plans to ease curbs on housing purchases by non-local buyers. The PBOC indicated a plan to cut the outstanding mortgage rate by another 50 basis points and reduce the minimum downpayment ratio for second-home purchase from 25% to 15%. In its September politburo statement, China’s top leaders vowed to stabilise the property sector and prevent further declines. Shortly after, the Ministry of Finance announced that local governments could issue special-purpose bonds to acquire commercial properties for affordable housing and to purchase idle land from developers. The credit quota for “Project Whitelist” program was also doubled to RMB 4 trillion.

At the latest parliamentary meeting in March 2025, the National People’s Congress (NPC) opted not to introduce new initiatives, but instead called for better implementation of existing steps. This included city-specific relaxation of regulations, urban town renovations and giving local officials more autonomy in handling unsold homes. The NPC also emphasised the “effective preventing the risk of developers’ debt default”.

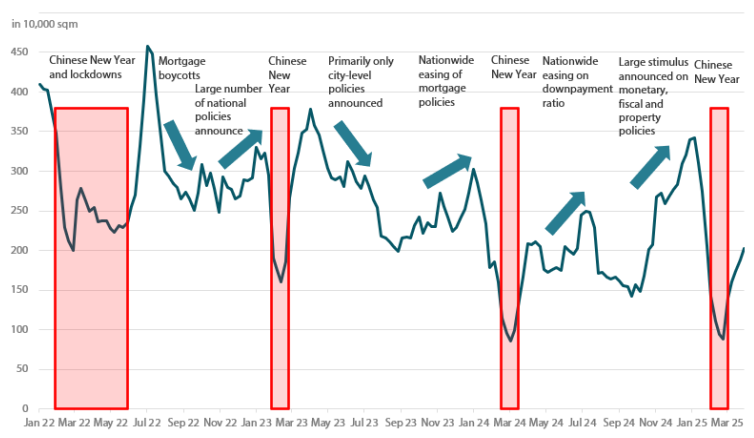

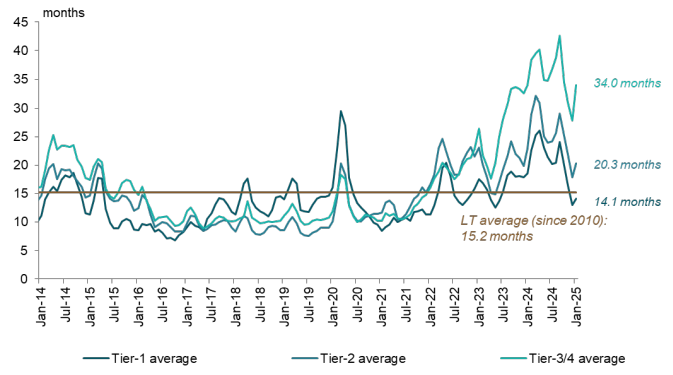

Chart 1 shows several inflection points in property sales following the announcement of “outsized” stimulus measures. Property sales swiftly rebounded after the announcement of demand-side easing measures, although the bounce was short-lived. Towards the end of 2024, some signs of recovery in the market were seen, with sales rebounding strongly since October thanks to the large stimulus packages announced in September. This recovery has continued into the first quarter of 2025, lasting more than six months, although improvements are more prominent in top tier cities. Housing inventories in Tier 1 cities have corrected to a relatively healthy level after strong sales in past few months, as shown in Chart 2.

Chart 1: 30 cities weekly property sales by gross floor area (4-week moving average)

Source: Wind, Bloomberg, Reuters, PBOC announcements, Nikko AM, March 2025

Chart 2: Inventory of 80 key cities (months)

Source: CRIC (China Real Estate Information Corp), Citi

On 2 April 2025, US President Donald Trump announced larger-than-expected global reciprocal tariffs on imports into the US. After imposing an additional tariff of 34% on imports from China on 2 April, Washington has significantly raised the levies, which now exceed 100%. We see risk of home sales in China pull back in the coming months amid arising challenges from internal and external headwinds such as tariffs. At the same time, we also expect the Chinese government to escalate its easing measures to revive and stabilise the property market should the sector’s outlook deteriorate materially.

Navigating Chinese property developer bonds in a new era of tighter government control

In an era of proactive government intervention and structural changes, could China’s troubled property sector be turning a corner? In our view, recovery will take time and be uneven, with top-tier cities expected to lead the way. Prior to the announcement of reciprocal tariffs from the US, there were early signs of stabilisation in top-tier cities. However, we see home sales rebounding only to face near term pressure amid heightened trade tensions and economic uncertainties. We also believe that a sustained recovery—especially on mid- and lower-tier cities—will take time for the government’s policies to have a broader impact on the overall economy and property market. The initiative in which local governments purchase unsold homes for affordable housing, if carried out at the right scale, could speed up the destocking of inventory. However, the execution process will have to be monitored closely.

As shown in Chart 3, Chinese high-yield bonds have recovered sharply. This recovery can be attributed to factors including the significantly lower default rate seen in recent years and the Politburo’s strong commitment to stabilise the property sector, in addition to the property easing measures implemented by the government. In fact, in 2024 Chinese high-yielding bonds emerged as the best-performing sector in the Asia credit market, generating a 44% return at the index level, according to the J.P. Morgan Asia Credit Index.

Chart 3: Chinese property high-yield bonds (average price, USD)

Source: Bloomberg, Nikko AM, March 2025

We remain constructive on the Chinese real estate sector from a credit perspective, as we expect the government to maintain its supportive stance. We also anticipate default rates to continue decreasing, and we expect funding support for surviving names to continue. Looking at the surviving developers present in the offshore dollar market, many of these entities are backed by state-owned enterprises (SOEs). In contrast with private developers, these SOEs tend to benefit during industry downturns and periods of policy relaxations. This is because they can grab more market share from homebuyers by leveraging their stronger land banks and higher levels of trust among homebuyers. In recent years, we have seen diverging contracted sales performance between SOE-backed and privately-owned enterprise developers, and we expect the trend to continue.

Access to bank loans in the Chinese real estate sector has also improved since 2024. The relaxation of the restriction on the UOP for commercial property operating loans has significantly extended liquidity support for surviving developers with commercial property portfolios. The sector’s yields are likely to continue compressing over time, given the absence of supply and the reduced default rates in the sector, although volatility is expected to persist.

In the near term, a key focal point is major Chinese real estate developer Vanke, which has been facing tight liquidity and a significant maturity wall for its public bonds. Recent steps taken by the local government, including a management reshuffle and financing support, indicate efforts to address Vanke’s liquidity concerns. The local government’s approach towards Vanke is being closely watched by the market, especially after the latest NPC called for the prevention of developer debt defaults.

It remains to be seen if China’s property sector has bottomed out, but we continue to look out for further signs of more policy easing and a recovery in fundamentals. Chinese property bonds performed well in 2024, but sustained efforts are needed to stabilise the real estate market and prevent further declines. While some factors are beyond our control, investors can play an important role through credit selection, identifying the better-performing developers with favourable risk-reward profiles.

Any reference to a particular security is purely for illustrative purpose only and does not constitute a recommendation to buy, sell or hold any security. Nor should it be relied upon as financial advice in any way.